Beyond the Basics: Understanding the 10 GAAP Accounting Principles and Their Real-World Business Impact

Latest Update – July 2026

Financial reporting expectations continue to evolve as accounting standards and business models become more complex. The FASB Accounting Standards Codification remains the authoritative source of nongovernmental U.S. GAAP, making consistent accounting policies and sound documentation essential for finance teams.

Quick Answer

Generally Accepted Accounting Principles (GAAP) are the standardized rules U.S. businesses use to record, report, and present financial information consistently. GAAP matters beyond compliance: it's what makes your financial statements comparable year over year, credible to lenders and investors, and reliable enough to build tax and growth decisions on.

A business that follows GAAP loosely — or not at all — ends up with books that look fine internally but fall apart under a loan review, an audit, or a due-diligence request. Working with a CPA-led bookkeeping team that applies GAAP correctly from the first transaction avoids that gap entirely.

Key Facts at a Glance

GAAP provides a common financial reporting framework for U.S. businesses that follow generally accepted accounting principles. Its practical value extends beyond compliance because consistent accounting treatment improves financial comparisons, audit readiness, and management visibility.

The Financial Accounting Standards Board establishes and improves financial accounting and reporting standards for entities that follow U.S. GAAP. The FASB Accounting Standards Codification is the authoritative source of nongovernmental U.S. GAAP.

Quick Read

- GAAP supports consistent and comparable financial reporting.

- Ten core principles explain the practical foundation of GAAP.

- Consistency affects close processes, reporting, and financial analysis.

- Revenue and expense timing can materially change reported results.

- Documentation supports audits and accounting policy decisions.

- GAAP and statutory accounting serve different reporting purposes.

Introduction

Accounting problems rarely begin with the financial statements themselves. They usually start earlier: an expense posted to the wrong period, inconsistent revenue treatment, an undocumented estimate, or a change in accounting methodology that no one clearly communicated.

These issues become visible during month-end close, audit preparation, lender reporting, or financial analysis. By then, accounting teams may spend hours tracing transactions and explaining why current results do not align with prior periods.

The 10 GAAP principles provide a foundation for preventing many of these inconsistencies. Rather than treating GAAP as a technical checklist used only by accountants, business leaders can view these principles as practical guidelines for producing financial information that is reliable, understandable, and useful for decision-making.

What Is GAAP and Why Does It Exist?

GAAP exists to solve one problem: without a shared standard, every business could report its numbers however it wanted, and financial statements would be meaningless to anyone outside the company. GAAP creates a common language — so a bank, an investor, or the IRS can look at your financials and trust that "revenue" means the same thing it means on every other GAAP-compliant statement they've ever reviewed.

This is also where GAAP and tax reporting diverge. GAAP governs how you present financial performance; tax rules govern what you owe. The two frequently produce different numbers for the same transaction, which is exactly why bookkeeping and tax filing need to be handled by people who understand both systems, not just one.

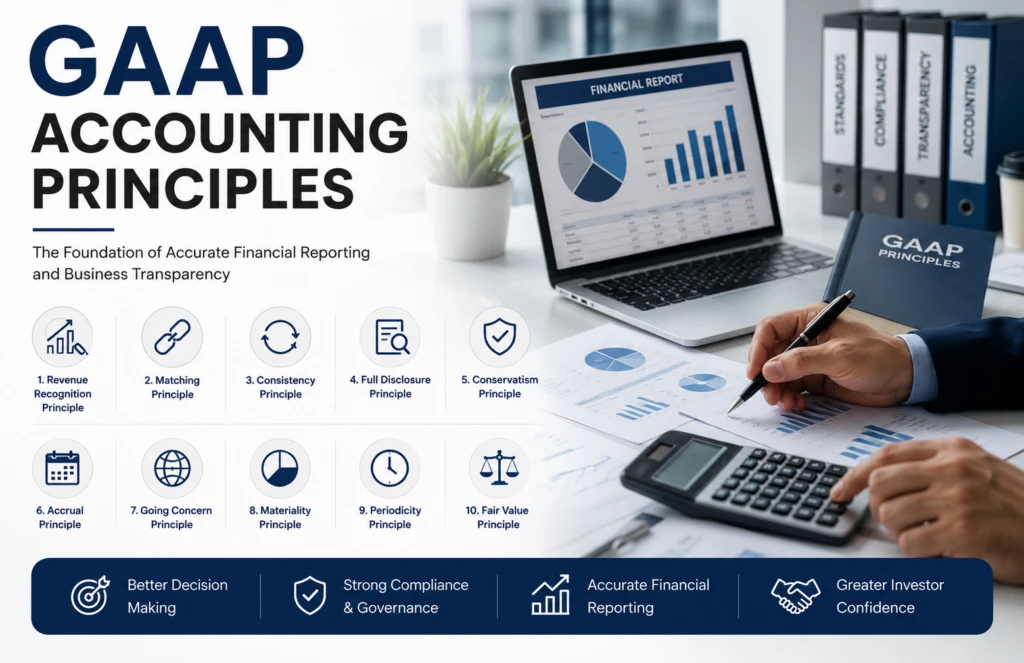

What Are the 10 GAAP Accounting Principles?

The principles below explain the fundamental ideas behind consistent financial reporting. Their value becomes clearer when viewed through everyday accounting operations rather than textbook definitions.

1. Principle of Regularity

Accountants are expected to follow established GAAP rules and standards consistently. Accounting treatment should not be changed simply because another method produces a more favorable financial result.

Operationally, this requires clear accounting policies. Revenue recognition, expense classification, capitalization, and account reconciliation practices should follow documented procedures rather than individual preference.

2. Principle of Consistency

A business should apply the same accounting methods from one reporting period to another. Consistency allows management, investors, and other users to make meaningful comparisons.

Suppose a company changes its inventory valuation or depreciation methodology. The accounting team must evaluate the reporting implications and provide appropriate disclosure when required. Unexplained changes can distort trends and create additional work during audits.

3. Principle of Sincerity

Financial reporting should represent the company's financial position fairly and in good faith. Accountants should apply professional judgment objectively rather than deliberately shaping results to meet a preferred narrative.

This principle becomes especially relevant when estimates are involved. Allowances, reserves, and impairment assessments should be supported by reasonable assumptions and documentation.

4. Principle of Permanence of Methods

Accounting methods should remain stable enough to support comparison over time. While similar to consistency, permanence emphasizes maintaining established financial reporting procedures unless a justified change is necessary.

Frequent changes in account mappings, close procedures, or reporting classifications can create reconciliation problems. Stable methods make financial review more efficient and reduce confusion across reporting periods.

5. Principle of Non-Compensation

Assets and liabilities, as well as income and expenses, should generally be reported separately rather than improperly offset to hide financial details.

For example, a company should not simply net unrelated expenses against revenue to make performance appear stronger. Proper presentation gives financial statement users a clearer understanding of the underlying activity.

6. Principle of Prudence

Accounting judgments should be made carefully and should not overstate financial performance or asset values. Prudence becomes particularly important when uncertainty affects estimates.

A finance team reviewing potentially uncollectible receivables, for instance, should consider realistic collection expectations. Ignoring clear credit risks may overstate assets and create an unpleasant correction in a later reporting period.

7. Principle of Continuity

Financial reporting generally assumes that a business will continue operating for the foreseeable future unless evidence suggests otherwise.

This going-concern assumption affects how assets, liabilities, and long-term obligations are viewed. Significant liquidity problems or other conditions may require management and accounting professionals to evaluate whether additional analysis or disclosure is necessary.

8. Principle of Periodicity

Financial activity is divided into standard reporting periods (monthly, quarterly, annually), which is what makes trend analysis and year-over-year comparison possible in the first place. This is also why monthly bookkeeping matters more than an annual scramble — periodicity only works if the underlying records are kept current throghout the year.

9. Principle of Materiality

Financial reporting should give proper attention to information that could influence users' decisions. Not every small accounting difference requires the same level of investigation or treatment.

Materiality requires judgment. Finance teams often consider the size and nature of an item when evaluating errors, adjustments, or disclosures. A seemingly small issue may still matter if it affects compliance, changes a key trend, or involves unusual activity.

10. Principle of Utmost Good Faith

Parties involved in financial reporting are expected to act honestly and provide relevant information openly. Important financial facts should not be intentionally concealed from stakeholders.

For accounting teams, good faith also depends on communication. Unusual transactions, contract changes, and significant estimates should reach the people responsible for financial reporting before the close is completed.

Together, the 10 GAAP principles shape the discipline behind reliable accounting. Their practical effect can be seen in close schedules, account reconciliations, policy documentation, management reporting, and audit support.

The Real-World Impact of GAAP on Accounting Operations

The GAAP accounting principles influence far more than year-end financial statement preparation. They affect everyday decisions about when transactions are recorded, how accounts are classified, and what supporting documentation should be retained.

Consider month-end close. A controller reviewing revenue may discover that one business unit recorded contract income when an invoice was issued, while another used a different recognition point. Even if both teams believe their approach is reasonable, inconsistent treatment creates reporting risk and additional reconciliation work.

The same problem appears with expenses. Missing accruals can make one month's profitability look unusually strong and the following month unexpectedly weak. Management may then spend time investigating a business performance issue that is actually an accounting timing problem.

Applying the 10 GAAP principles consistently helps finance teams build repeatable accounting processes. Close checklists, account ownership, documented accounting policies, and review controls turn broad accounting concepts into daily operating practices.

Why GAAP Matters for Financial Decision-Making

Financial statements influence budgeting, cash planning, lending discussions, investment decisions, and performance reviews. When accounting treatment changes unpredictably, decision-makers lose confidence in the numbers.

A CFO comparing gross margin across six months needs reasonable assurance that revenue and related costs were treated consistently. A lender reviewing financial statements needs information prepared under an understandable reporting framework. An accounting manager preparing for an audit needs documentation supporting significant judgments and balances.

The phrase accepted accounting principles GAAP is sometimes treated as a compliance concept, but the operational value is broader. A disciplined accounting framework improves the quality of financial conversations because teams spend less time debating how numbers were produced and more time understanding what those numbers indicate.

GAAP and Statutory Accounting: Why the Difference Matters

The discussion around statutory accounting principles vs GAAP is particularly relevant to insurance organizations. These frameworks have different reporting objectives and should not be treated as interchangeable.

U.S. GAAP generally focuses on providing useful financial information to investors and other financial statement users. Statutory accounting principles, by comparison, place greater emphasis on an insurer's balance sheet and ability to meet policyholder obligations.

For finance teams working with multiple reporting requirements, the difference can create additional reconciliation and documentation demands. The same underlying financial activity may require different treatment or presentation depending on the reporting framework.

Understanding the reporting purpose first helps teams establish appropriate account mappings, adjustment processes, and review controls.

Common Challenges When Applying GAAP

Knowing accounting principles is different from applying them consistently across a growing organization. Problems often emerge when transaction volume increases faster than accounting processes mature.

One common issue is inconsistent documentation. A significant accounting judgment may be discussed during a meeting but never formally recorded. Months later, the accounting team may struggle to explain the treatment during an audit or management review.

Close pressure creates another challenge. Vendor reconciliation delays, late invoices, incomplete expense data, and last-minute journal entries can make accurate cutoff difficult. Teams working against tax or reporting deadlines may also rely on manual workarounds that increase the risk of errors.

Scalability matters as well. An accounting process that worked with 200 monthly transactions may become unreliable at 5,000 transactions. Applying the 10 GAAP principles effectively requires processes, controls, and review procedures that evolve with the business.

How Stratax Advisors Helps

Stratax Advisors supports businesses in strengthening accounting workflows, financial reporting, reconciliations, and compliance-focused processes. The work begins with understanding how financial information moves through the organization, from transaction recording and account classification to close and reporting.

Our professionals help identify reporting inconsistencies, reconciliation gaps, and process weaknesses that can affect financial accuracy. We support structured close procedures, account reviews, financial reporting, and documentation practices designed to improve visibility and execution.

For businesses managing complex accounting requirements, Stratax Advisors also helps establish more repeatable workflows. The goal is practical: cleaner financial information, fewer unexplained adjustments, better reporting consistency, and stronger support for management and compliance needs.

Conclusion

GAAP becomes most valuable when accounting principles are reflected in daily processes. Consistent transaction treatment, careful cutoff, documented judgments, and reliable review procedures determine whether financial reports can genuinely support business decisions.

As companies grow, accounting complexity rarely remains static. New revenue arrangements, systems, reporting expectations, and transaction volumes create new pressure on finance teams. A strong understanding of the 10 GAAP principles gives businesses a durable foundation for adapting their accounting processes without sacrificing reporting quality.

Frequently Asked Questions :

Business owners do not need to become technical accountants, but understanding the purpose of GAAP helps them interpret financial reports and ask better questions. Accounting decisions affect reported revenue, expenses, assets, and profitability. Basic awareness also helps leaders recognize why consistent processes and documentation matter when evaluating financial performance.

Yes. If revenue, expenses, or other transactions are treated differently across reporting periods, financial trends may become misleading. Management might interpret an accounting timing difference as a change in operating performance. Consistent methods make comparisons more meaningful and give finance leaders a stronger basis for budgeting, forecasting, and performance analysis.

Teams apply GAAP through cutoff reviews, accruals, reconciliations, journal entry controls, account analysis, and financial statement review. The GAAP accounting principles become practical when supported by close checklists and documented policies. These processes help identify missing transactions, unusual balances, and inconsistent accounting treatment before reports are finalized.

No. When comparing statutory accounting principles vs GAAP, the reporting objectives differ. GAAP generally provides financial information for investors and other financial statement users, while statutory accounting emphasizes insurer solvency and policyholder protection. Insurance finance teams may therefore need processes for identifying, documenting, and reconciling differences between reporting frameworks.

Documentation explains how significant accounting decisions were reached and provides support during financial reviews or audits. When teams discuss a judgment but fail to record the reasoning, future reviewers may struggle to understand the treatment. Strong documentation also supports consistent application of accepted accounting principles GAAP as staff, systems, and business activities change.

About the Author

Daniel (“Dan”) T. Jones, CPA brings over 40 years of experience in finance, management, and advisory services to Stratax Advisors. He works closely with privately owned growth companies, business owners, and high-net-worth individuals, providing business, tax, and financial planning support across industries including real estate, manufacturing, retail, and professional services. A former KPMG partner, Dan has also founded and led multiple successful entrepreneurial ventures in real estate and financial services. He holds a B.S. with honors in Business Administration and Accounting from the University of North Carolina at Chapel Hill and is actively involved in community leadership.

Let’s Take Our Conversation Ahead

At Stratax, we empower individuals and businesses to make confident financial decisions. With deep expertise and unwavering precision, we deliver solutions that safeguard your future and accelerate your success.

Schedule a Meeting